{kind=link}

Banks and credit score unions provide financial savings accounts and CDs. Brokers equivalent to Vanguard, Constancy, and Charles Schwab provide cash market funds and Treasuries. They serve related functions at a excessive degree. Each a financial savings account and a cash market fund permit versatile deposits and withdrawals. Each CDs and Treasuries provide a hard and fast rate of interest for a hard and fast time period.

| Banks and Credit score Unions | Brokers | |

|---|---|---|

| Versatile Deposits and Withdrawals | Excessive Yield Financial savings Account | Cash Market Fund |

| Mounted Time period | CDs | Treasuries |

Whereas most discussions on these merchandise from banks and brokers focus on having FDIC insurance coverage or not (see No FDIC Insurance coverage – Why a Brokerage Account Is Secure), many individuals don’t notice that there’s a elementary distinction between the roles banks and brokers play. I discussed this distinction in my Information to Cash Market Fund & Excessive Yield Financial savings Account. It’s price highlighting it once more.

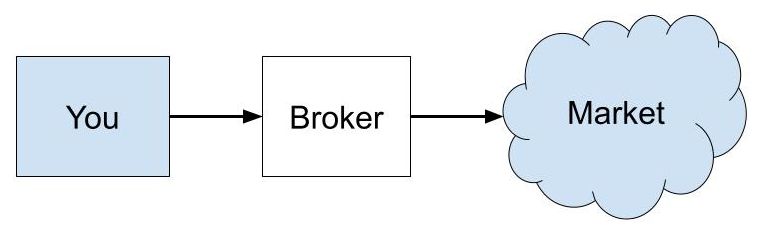

The elemental distinction is that banks and credit score unions provide a two-party personal contract whereas a dealer serves as an middleman between you and the general public market.

Two-Get together Personal Contract

A two-party personal contract means something goes so long as one social gathering makes the opposite social gathering comply with the phrases. If a financial institution will get you to comply with a 0.04% fee in a financial savings account or a 0.05% fee in a 10-month CD (these are precise present charges from a big financial institution), that’s what you’ll get no matter what the speed ought to be. The financial institution units the speed. They don’t must justify it. You get a foul contract should you aren’t conscious of the going fee.

A foul contract doesn’t need to be this apparent. It’s been over a yr now because the Fed raised the short-term rates of interest above 5%. The speed on a “good” on-line high-yield financial savings account such because the one from Ally Financial institution is at the moment 4.2% whereas a cash market fund pays 5% or extra. It’s 4.2% from the financial institution solely as a result of the financial institution says so. You’re paying a “familiarity penalty” if you stick with Ally.

I’m not choosing on Ally particularly. It really works the identical at Marcus, Synchrony, Amex, Uncover, Capital One, or Barclays. Ken Tumin, the founding father of DepositAccounts.com, made this commentary in April 2024:

If you happen to take a step again and ask why banks can profit from buyer inertia within the first place, you notice that’s the character of a two-party personal contract. Prospects should take the initiative to interrupt out of a foul contract.

Some banks play methods by providing a brand new financial savings account underneath a special identify with aggressive charges whereas preserving the speed low on the prevailing financial savings accounts. The speed is low on the prevailing account solely as a result of that’s the contract you agreed to. The financial institution isn’t obligated to maneuver you to the brand new program as a result of that’s not within the contract. Nor does the financial institution need to let you know that you may change to the brand new program to get the next fee. It’s as much as you to seek out out and take motion.

Charges at many massive credit score unions aren’t any higher. I’m a member of a well-regarded credit score union. It’s the most important credit score union within the nation by far, with 3 times the belongings of the second-largest credit score union. The speed on its financial savings account is 1.5% when you’ve gotten $50,000 within the account. That’s 3.5% decrease than the yield in a cash market fund.

A very good contract right now can flip into a foul contract tomorrow. How the contract will change is within the contract itself. A financial institution presents 5.0% APY on a 13-month CD right now. That’s an OK fee however what occurs after 13 months? You agree within the contract it should routinely renew to a 12-month CD at a fee set by the financial institution at the moment except you are taking particular actions to cease it inside a brief window. Guess what fee the financial institution will set on its 12-month CD? Nearly at all times a foul one. It really works this manner since you agreed to the contract.

When you’ve gotten a two-party personal contract, your curiosity is in direct battle with the opposite social gathering within the contract. The onus is on you to know whether or not the contract is sweet or unhealthy. It’s on you to observe when an excellent contract turns into a foul contract. Caveat emptor. You’ll have to leap from contract to contract should you don’t need to get caught in a foul contract.

Some persons are extra alert in monitoring and leaping. They’ve an opportunity to “beat the market” however they pay for it with a heavy psychological workload and time spent on opening new accounts and shutting outdated accounts. Many fail to be vigilant sooner or later. They begin paying the “familiarity penalty” as a result of it’s too tiring in any other case.

Market Middleman

A dealer acts as an middleman. They get you the market fee and take a lower. A dealer doesn’t set the speed. The market does. The dealer solely units its lower.

A cash market fund will get you the market fee on cash market securities minus the lower by the fund supervisor. Some fund managers take a much bigger lower than others however the distinction between main gamers is way smaller and extra steady than the distinction between charges supplied by completely different banks and credit score unions. If you happen to use a cash market fund with the smallest lower, equivalent to one from Vanguard, you nearly assure you’ll have the very best fee in a cash market fund always.

You continue to pay a “familiarity penalty” if you use a cash market fund from Constancy or Schwab versus one from Vanguard however the distinction is within the 0.2%-0.3% vary whereas the “familiarity penalty” in financial institution financial savings accounts may be greater than 1%. The “familiarity penalty” is zero or negligible in shopping for Treasuries by means of Constancy, Schwab, or Vanguard.

Treasuries don’t trick you into renewing at a foul fee. They routinely pay out at maturity. You’ll get the market fee if you purchase once more. If the dealer presents the “auto roll” characteristic and also you allow it at your selection, your Treasuries will routinely renew on the market fee. You possibly can relaxation assured that you just gained’t be cheated.

Cash market funds and Treasuries paid little or no when the Fed stored rates of interest at zero and ran a number of rounds of Quantitative Easing a number of years in the past. That wasn’t cash market funds’ fault or brokers’ fault. These have been the market charges at the moment. Like investing in index funds, you hand over the dream of “beating the market” if you put your cash in cash market funds and Treasuries however you additionally constantly get the market charges always. It doesn’t require preserving your guard up, monitoring rigorously, or leaping.

If you wish to constantly earn an excellent yield with low upkeep, ditch banks and credit score unions. If you happen to usually hold cash in a financial savings account at a financial institution or a credit score union, put the cash in a cash market fund at a dealer. Listed below are some decisions at Vanguard, Constancy, and Schwab:

These are good beginning factors. You will discover more cash fund decisions in Which Vanguard Cash Market Fund Is the Greatest at Your Tax Charges, Which Constancy Cash Market Fund Is the Greatest at Your Tax Charges, and Which Schwab Cash Market Fund Is the Greatest at Your Tax Charges.

If you happen to usually purchase a CD from a financial institution or a credit score union, purchase a Treasury of the identical time period at Vanguard, Constancy, or Schwab. See How To Purchase Treasury Payments & Notes With out Payment at On-line Brokers and The way to Purchase Treasury Payments & Notes On the Secondary Market.

I used to have many accounts with banks and credit score unions. I’ve solely $60 in financial institution accounts now. My money is in cash market funds and Treasuries in a Constancy brokerage account. Bank card payments routinely debit Constancy on the due date. Constancy routinely sells a cash market fund to cowl the debits. See 2 Methods to Use Constancy as a Financial institution Account.

The Fed has signaled that they might decrease rates of interest quickly. I don’t suppose they may lower charges all the best way again to zero once more. If in the future banks and credit score unions begin paying extra on their financial savings accounts and CDs than cash market funds and Treasuries, which I doubt will occur, I’ll nonetheless stick with cash market funds and Treasuries as a result of I just like the transparency and equity. I’d relatively get the market fee always than depend on the benevolence of a financial institution or a credit score union.

Say No To Administration Charges

In case you are paying an advisor a share of your belongings, you might be paying 5-10x an excessive amount of. Discover ways to discover an unbiased advisor, pay for recommendation, and solely the recommendation.