Projection")

{kind=link}

Retirees on Social Safety obtain a rise of their Social Safety advantages every year often known as the Price of Dwelling Adjustment or COLA. The COLA was 3.2% in 2024. Retirees on Social Safety will as soon as once more obtain a COLA in 2025 nevertheless it gained’t be as massive because the one in 2024 as a result of inflation has cooled down.

Computerized Hyperlink to Inflation

Some retirees assume the COLA is given on the discretion of the President or Congress they usually need their elected officers to handle seniors by declaring a better COLA. They blame the President or Congress once they assume the rise is just too small.

It was achieved that means earlier than 1975 however the COLA has been robotically linked to inflation for practically 50 years. How a lot the COLA will probably be is set strictly by the inflation numbers. The COLA is excessive when inflation is excessive. It’s low when inflation is low. There’s no COLA when inflation is zero or destructive, which occurred in 2010, 2011, and 2016.

CPI-W

Particularly, the Social Safety COLA is set by the rise within the Shopper Worth Index for City Wage Earners and Clerical Staff (CPI-W). CPI-W is a separate index from the Shopper Worth Index for All City Customers (CPI-U), which is extra usually referenced by the media once they speak about inflation.

CPI-W tracks inflation skilled by staff. CPI-U tracks inflation skilled by customers. There are some minor variations in how a lot weight totally different items and providers have in every index however CPI-W and CPI-U look virtually equivalent while you put them in a chart.

The purple line is CPI-W and the blue line is CPI-U. They differed by solely smidges in 30 years.

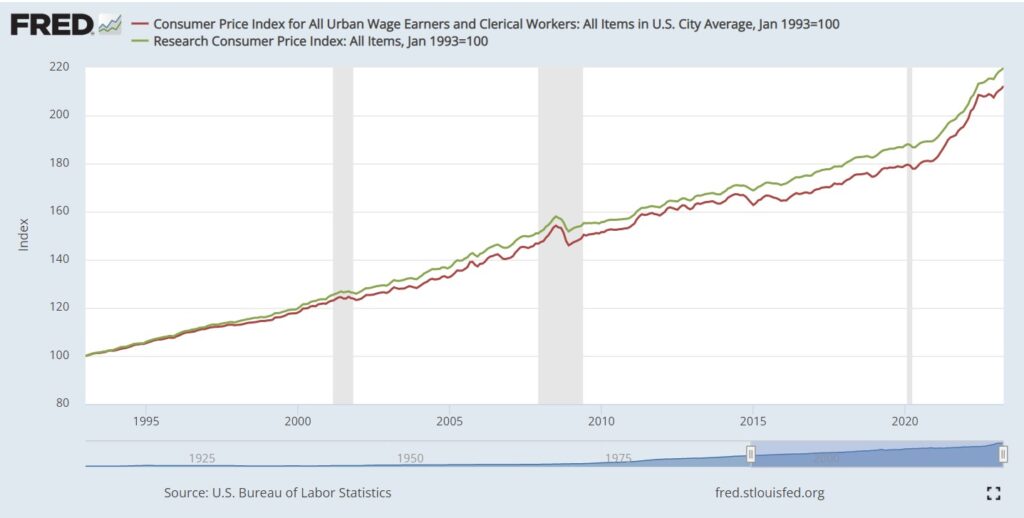

There’s additionally a analysis CPI index known as the Shopper Worth Index for People 62 years of age and older, or R-CPI-E. This index weighs extra by the spending patterns of older People. Some researchers argue that the Social Safety COLA ought to use R-CPI-E, which has elevated greater than CPI-W within the final 30 years.

The inexperienced line is R-CPI-E. The purple line is CPI-W. R-CPI-E outpaced CPI-W in 30 years between 1993 and 2023 however not by a lot. Had the Social Safety COLA used R-CPI-E as an alternative of CPI-W, Social Safety advantages would’ve been greater by 0.1% per yr, or a bit over 3% after 30 years. That’s nonetheless not a lot distinction.

No matter which actual CPI index is used to calculate the Social Safety COLA, it’s topic to the identical general value atmosphere. Congress selected CPI-W 50 years in the past. That’s the one we’re going with.

Q3 Common

Extra particularly, Social Safety COLA for subsequent yr is calculated by the rise within the common of CPI-W from the third quarter of final yr to the third quarter of this yr. You get the CPI-W numbers in July, August, and September. Add them up and divide by three. You do the identical for July, August, and September final yr. Examine the 2 numbers and around the change to the closest 0.1%. That’ll be the Social Safety COLA for subsequent yr.

2025 Social Safety COLA

We gained’t have all of the CPI-W information for Q3 2024 till October 10, 2024 however we are able to make projections primarily based on the info now we have now.

If shopper costs in September 2024 keep on the identical stage as in August 2024, the 2025 Social Safety COLA will probably be 2.4%.

If shopper costs in September 2024 go up at a tempo of three% annualized (roughly 0.25% per 30 days), the 2025 Social Safety COLA will probably be 2.5%.

I estimate that the 2025 Social Safety COLA will probably be 2.5%. That is decrease than the three.2% Social Safety COLA in 2024 as a result of inflation has come down.

Medicare Premiums

Should you’re on Medicare, the Social Safety Administration robotically deducts the Medicare premium out of your Social Safety advantages. The Social Safety COLA is given on the “gross” Social Safety advantages earlier than deducting the Medicare premium and any tax withholding.

Medicare broadcasts the premium for subsequent yr across the identical time Social Safety broadcasts the COLA however not essentially on the identical day. The rise in healthcare prices is a part of the price of residing that the COLA is meant to cowl. You’re nonetheless getting the total COLA despite the fact that part of the COLA will probably be used towards the rise in Medicare premiums.

Retirees with a better revenue pay greater than the usual Medicare premiums. That is known as Revenue-Associated Month-to-month Adjustment Quantity (IRMAA). I cowl IRMAA in 2024 2025 2026 Medicare IRMAA Premium MAGI Brackets.

Root for a Decrease COLA

Individuals intuitively need a greater COLA however a better COLA can solely be brought on by greater inflation. Greater inflation is dangerous for retirees.

Whether or not inflation is excessive or low, your Social Safety advantages could have the identical buying energy. It’s best to assume extra concerning the buying energy of your financial savings and investments outdoors Social Safety. When inflation is excessive, despite the fact that your Social Safety advantages get a bump, your different cash loses extra worth to inflation. Your financial savings and investments outdoors Social Safety will last more when inflation is low.

You need a decrease Social Safety COLA, which implies decrease inflation and decrease bills.

Some individuals say that the federal government intentionally under-reports inflation. Even when that’s the case, you continue to need a decrease COLA.

Suppose the true inflation for seniors is 3% greater than the inflation numbers reported by the federal government. Should you get a 3% COLA when the true inflation is 6% and also you get a 7% COLA when the true inflation is 10%, you’re a lot better off with a decrease 3% COLA along with 6% inflation than getting a 7% COLA along with 10% inflation. Your Social Safety advantages lag inflation by the identical quantity both means, however you’d somewhat your different cash outdoors Social Safety loses to six% inflation than to 10% inflation.

Root for decrease inflation and decrease Social Safety COLA if you end up retired.

Say No To Administration Charges

In case you are paying an advisor a proportion of your belongings, you’re paying 5-10x an excessive amount of. Discover ways to discover an unbiased advisor, pay for recommendation, and solely the recommendation.